Last week saw the clearing of the 18th and 19th successful Capacity Market Auctions, procuring security of supply for Delivery Years 2025/26 and 2028/2029. The Capacity Market ensures that supply can meet demand by providing payments to ensure capacity is online and available to the grid when needed. The Electricity Settlements Company (LCCC’s sister company) is the Settlement Body for the Capacity Market, and amongst other responsibilities, completes checks on set-ups and data requirements, ensures accurate settlement of System Stress Events and acts as trusted advisors to DESNZ and Ofgem.

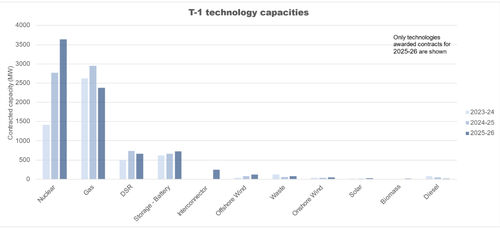

The T-1, which acts as a top-up Auction to the previous T-4, procured its highest ever capacity of 8019MW across 246 providers; and alongside the previous T-4 capacity procured, this will ensure security of supply from 1 October 2025/2026. It was noticeable within the latest Auction that gas was no longer the largest constituent, whereas since 2021/22 it has been the predominant generation type at both Auctions. Gas has fallen 19%, from 2945MW in 2024/25 to 2376MW, whereas nuclear rose by 31% from 2767MW in 2024/25 to 3636MW. Overall, gas is now 29.6% of the total awarded capacity and nuclear is 45.3%.

Outside of gas capacity, solar and wind (both offshore and onshore) saw a 60% increase from last year's T-1 Auction of 118MW to 188MW, although it is important to note that this makes up 2.3% of the total capacity awarded. There was also an increase in battery storage which was up 11.1% on 2024/25 to 728MW, although there was no pumped storage, meaning the total amount of storage has reduced by 13% since last year.

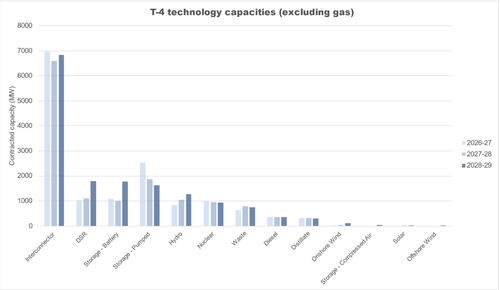

The T-4 Auction, which secures capacity four years ahead, procured 43,076MW across 669 providers, and is largely aligned with the last three T-4 Auctions. Similar to the T-1, gas dropped 4.8% from 2027/28 levels however, it is still by far the largest technology type, making up 63.3% of the capacity.

There was a similar increase in solar and wind (both offshore and onshore) as in the T-1, with 143MW of agreements, up from 49MW, making up 0.3% of the awarded T-4 capacity. Demand Side Response also increased in this Auction, making up 4.2% of awarded capacity, surging by 63.1% to 1789MW from 1097MW in 2027/28.

Another large increase in this year's T-4 Auction was battery storage, which was 75.4% up on last year's T-4, from 1016MW to 1782MW. Overall, storage rose by 18.9%, including the first compressed air project since before the pandemic.

Here at the Electricity Settlements Company, we are excited to start working with Capacity Providers to prepare for the 2025/26 Delivery Year. If you have any questions, feel free to contact us at info@electricitysettlementscompany.uk